Foreign Withholding Taxes on Dividends and your Investment Returns

January 2026

Introduction and Non-registered Accounts

Canadian individuals receiving dividends from Canadian companies receive a preferential income tax rate. While 138% of a public company dividend is reported on the tax return, a lucrative dividend tax credit reduces the individual tax rate. This dividend tax credit is used to recognize that corporations have already paid income taxes on income used to pay the dividend.

This preferential tax rate does not apply to dividends received by your RRSP or RRIF. Of course, there are no taxes paid by your RRSP/RRIF until the money is withdrawn from your account in the future, probably in retirement. At that time, your RRSP or RRIF withdrawal is fully taxable, just like interest income. As a side note, 50% of your capital gains are tax-free under current legislation; however, no break is received when capital gains are realized within your RRSP/RRIF. Again, this is because no taxes are paid until funds are withdrawn, which are then fully taxable.

The dividend preferential tax rate also does not apply to dividends received from foreign companies. Foreign dividends are converted to Canadian dollars and taxed in Canada at the same rate as interest income is reported. When the foreign companies to pay dividends to Canadians, a rate of 15% or 25% withholding tax is applied. This is the way that foreign countries collect income taxes from non-residents on income earned within their country. Canada uses the same method to tax non-residents.

On your Canadian tax return, you are able to claim a “foreign tax credit” to reduce your Canadian taxes by any amount of taxes paid to a foreign country. In certain cases, this tax deduction is changed to an income reduction, which does not result in a complete recovery of taxes. However, this tax credit system only applies to non-registered accounts. These foreign taxes will be reported separately on the T5 or T3 tax slip you receive for holdings of individual stocks, ETF’s, mutual funds and segregated funds.

Registered Retirement Accounts (RRSPs and RRIFs)

There are two scenarios to consider here. The first is investments in USA companies. The second is investment in non-USA companies, or investments in funds that have a combination of USA and other countries.

1) Investments in USA companies

· Individual stocks

If you file a special U.S. IRS form for your RRSP or RRIF with the brokerage firm, they are not required to withhold taxes because of a US-Canada agreement. The form is called a W8-BEN Certificate of Foreign Status of Beneficial Ownership for United States Tax Withholding and Reporting. This only applies to RRSPs or RRIF, and for individual stock holdings. If foreign taxes are not withheld, you need not worry about being taxed twice on the same income (i.e., by the USA and again by Canada).

· Exchange Traded Funds (ETFs) or Mutual Funds

When a USA company pays dividends on the shares held by an ETF or a mutual fund, they are paying those dividends to that fund company and not to an individual. If the USA company is paying dividends to a Canadian ETF or mutual fund, taxes will be withheld. The individual taxpayer is purchasing those USA company shares through that fund managed by the fund company, which is located in Canada. Hence, the individual has no direct contact with the USA company to ask them not to withhold dividends by filing a W8-BEN form. Consequently, any withholding taxes, typically 15%, withheld from dividends earned by the USA ETF or mutual fund cannot be recovered by your RRSP/RRIF. This may not be an issue if most of the earnings from that ETF or mutual fund is from capital gains and not from dividends. However, if there are substantial dividends earned, this would represent up to 15% additional taxes on top of the taxes you pay when you take the money out of your RRSP/RRIF in the future. It is best not to own USA dividend-paying ETFs or mutual funds within your RRSP or RRIF unless this double tax is too small to be of concern to you. There is one exception.

If you wish to hold a USA ETF in your RRSP or RRIF, and you purchase it from a USA Exchange (i.e., a USA Listed ETF), and you file the W8-BEN, then there will be no withholding taxes when that USA Listed ETF pays the dividends to your account.

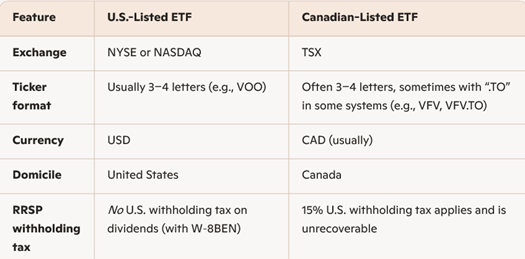

By way of example, the Vanguard VOO (Vanguard S&P 500 ETF) is a U.S.-listed ETF. It trades on the New York Stock Exchange (NYSE) in U.S. dollars. Because it is U.S.-listed holding, if VOO is inside an RRSP or RRIF, it qualifies for the Canada–U.S. tax treaty exemption from the 15% U.S. withholding tax on dividends as long as your broker has a valid W‑8BEN on file.

If you purchase the same fund on the Toronto Stock Exchange, it would be the Vanguard VFV (Vanguard S&P 500 Index ETF). It holds U.S.-listed VOO as its underlying asset. However, because it is Canadian-domiciled, the U.S. withholding tax on dividends cannot be avoided. This tax is embedded in the fund’s returns and is not recoverable.

The following is a table identifying differences between USA and Canadian-Listed ETFs held in an RRSP/RRIF:

2) Investments in foreign countries other than the USA, or an ETF/Mutual fund with holdings from a combination of USA and other countries

If you hold individual stocks from foreign companies other than the USA within your RRSP/RRIF, any foreign taxes withheld on dividends from the stocks will not be recoverable by way of a foreign tax credit, and will result in duplicate taxes. The first tax cost is the foreign withholding tax, and the second tax cost will occur when the money is removed from your RRSP/RRIF. In addition, if you hold ETF’s or mutual funds with investments in foreign countries other than the USA, including an international or global funds, any withholding taxes on dividends received will also not be recoverable. If you do not mind paying this extra level of tax, then for investments in foreign stocks other than the US, it is best to own Canadian-Listed ETFs. This will avoid a double layering of taxation. (For the US-Listed ETF, the non-USA foreign taxes withheld when paid to the USA ETF will not be recoverable, and further USA withholding taxes on this foreign income as it is paid to a Canadian resident will also not be recoverable.)

Registered Accounts other than RRSPs/RRIFs

Foreign taxes withheld from dividends paid to registered accounts such as TFSAs, RESP’s, RDSPs and FHSAs are treated the same as for RRSPs with one important exception. The Canada – USA tax treaty does not recognize these accounts and there is no exemption from withholding taxes on USA dividends paid to these accounts. Therefore, unless you are willing to pay additional taxes, no foreign holdings, including USA securities, should be held by these accounts, whether individual securities, ETF’s or mutual funds. For example, a dividend paid into your TFSA from a USA company will be subject to a 15% withholding tax, which will not be recoverable. This account is completely tax free from taxes on Canadian income, but you would be paying 15% taxes on your USA dividends.

Conclusion

The rules are complex. The loss of the dividend tax credit on foreign dividends in your non-registered accounts, and the loss of the foreign tax credit on foreign holdings in your registered accounts will affect your investment returns. The amount of this impact will depend on many issues, including the fixed income versus equity diversification of your investment portfolio, the allocation of your portfolio between growth versus dividend paying stocks, your decision on how much you wish to allocate to foreign countries instead of Canada, the placement of these securities between registered and non-registered accounts, and the extent to which you think the rate of return to be realized outside of Canada can beat that available in Canada (after taking into account the risks of foreign exchange and foreign issues) in spite of higher tax costs.

Always work with your advisors to reach decisions appropriate for you. Remember that the information in this article may have changed since it was written, and is my opinion only – your professionals may have other positions, and you should not rely solely on this information here.

Blair Corkum, CPA, CA, R.F.P., CFP, CFDS, CLU, CHS holds his Chartered Professional Accountant, Chartered Accountant, Registered Financial Planner, Chartered Financial Divorce Specialist as well as several other financial planning related designations. Blair offers hourly based fee-only personal financial planning, holds no investment or insurance licenses, and receives no commissions or referral fees. This publication should not be construed as legal or investment advice. It is neither a definitive analysis of the law nor a substitute for professional advice which you should obtain before acting on information in this article. Information may change as a result of legislation or regulations issued after this article was written.©Blair Corkum